Definition

For a stochastic process $(X_n)_{n\ge 0}$, the natural filtration up to time $n$ is

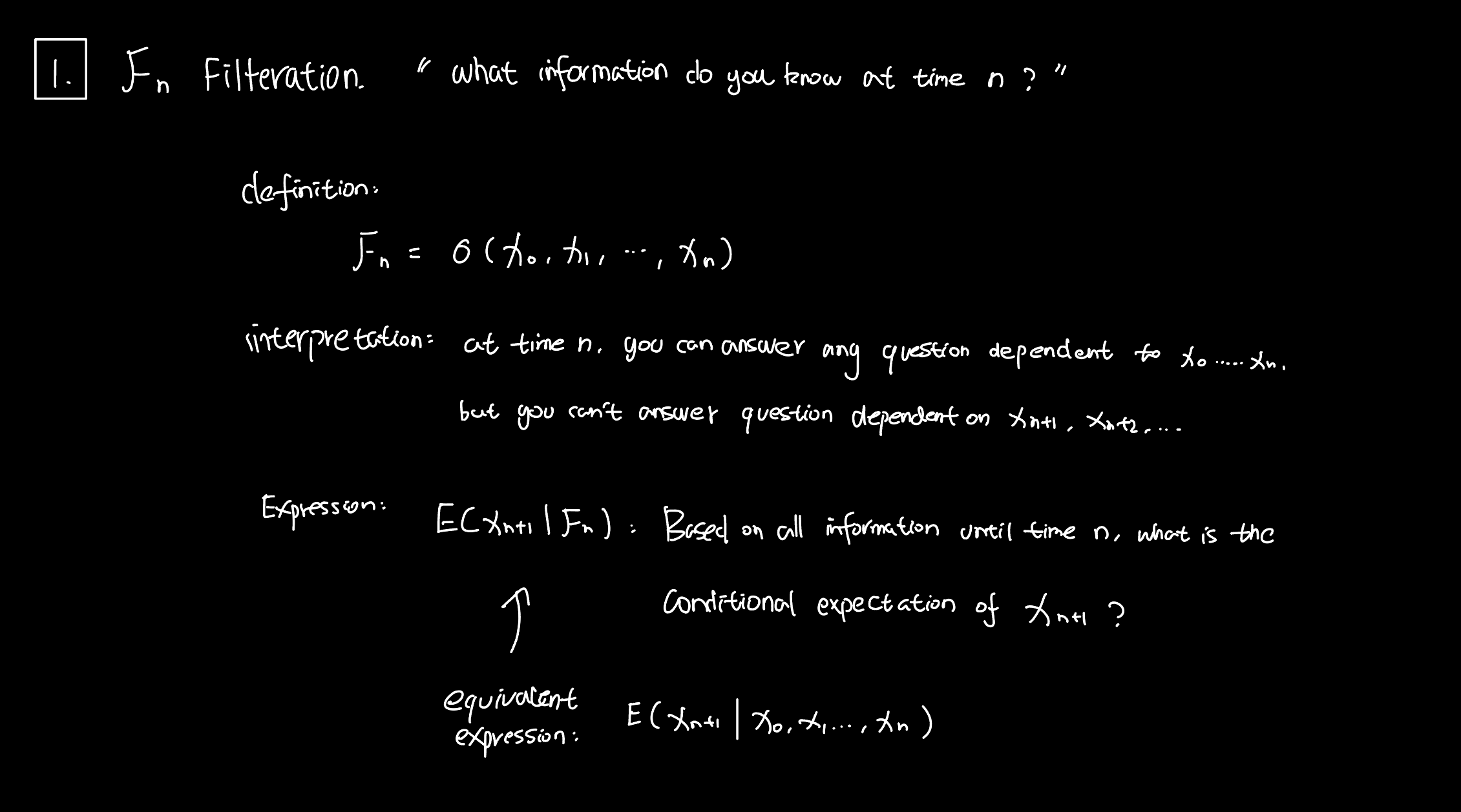

$$ \mathcal F_n=\sigma(X_0,X_1,\dots,X_n). $$More generally, a filtration is an increasing family of sigma-algebras

$$ \mathcal F_0\subseteq \mathcal F_1\subseteq \mathcal F_2\subseteq \cdots $$that records how available information grows over time.

Interpretation

$\mathcal F_n$ means all information revealed by time $n$.

If you know $\mathcal F_n$, then you can answer any question determined by $X_0,\dots,X_n$, but not questions that require future values such as $X_{n+1},X_{n+2},\dots$.

So a filtration formalizes the question:

What information is known at time $n$?

Conditional expectation with respect to a filtration

For an integrable random variable $Y$,

$$ \mathbb E(Y\mid \mathcal F_n) $$means the conditional expectation of $Y$ given all information available up to time $n$.

In particular,

$$ \mathbb E(X_{n+1}\mid \mathcal F_n) $$asks for the expected value of the next observation based on everything known up to time $n$.

When $\mathcal F_n=\sigma(X_0,\dots,X_n)$, this is equivalently written as

$$ \mathbb E(X_{n+1}\mid X_0,X_1,\dots,X_n). $$